Published on : 3/31/2025

KEY POINTS

- Equity markets stumbled in early 2025 as investors began to price in the risk of tariffs, rising recession probabilities, and elevated valuations, following two years of strong double-digit returns

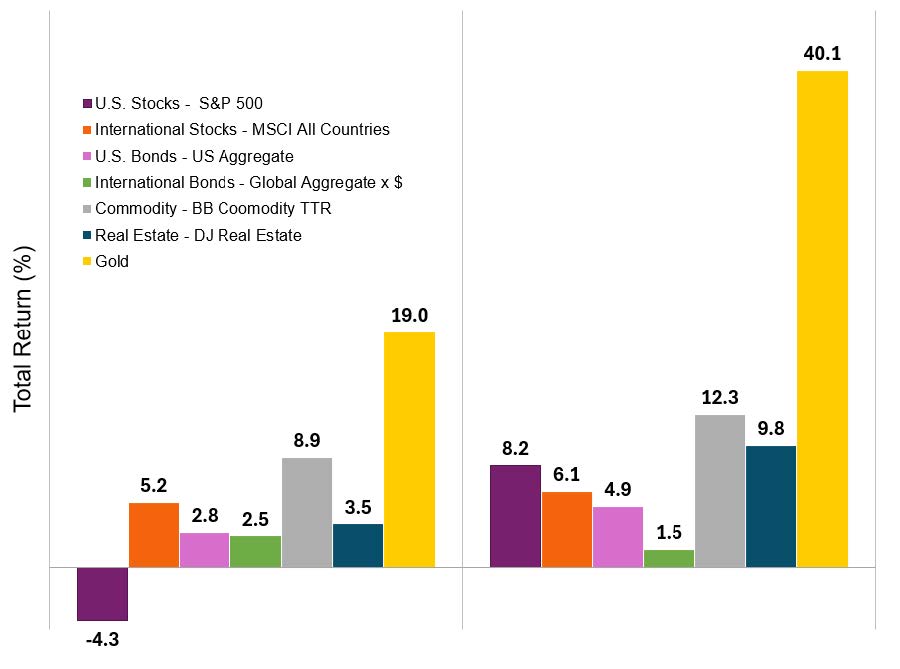

- The first quarter of 2025 highlighted the importance of diversification, as all major asset classes finished positive except for U.S. equities

- While GDP growth and unemployment numbers remain robust, core inflation continues to stay above the 2% target, presenting challenges for the broader economic outlook

THE ECONOMY

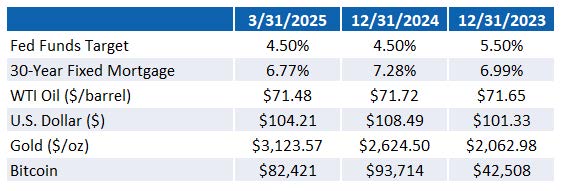

In the first quarter of 2025, the U.S. economy continued to demonstrate strong growth and a resilient labor market, consistently outperforming expectations. GDP growth remained solid, building on a 3.1% increase in the third quarter of 2024 and moderating slightly to the mid-2% range in the fourth quarter. The unemployment rate ticked up by 0.1 percentage points to 4.2%, while jobless claims remained at historically low levels. After showing signs of easing earlier in the year, disinflation appeared to stall in late 2024, with most price indices rising modestly but still well below their 2022 peaks. Despite the economy’s slight moderation, the Federal Reserve paused its rate cuts in January and adopted a more cautious stance, aiming to prevent a resurgence in inflationary pressures.

GLOBAL EQUITIES

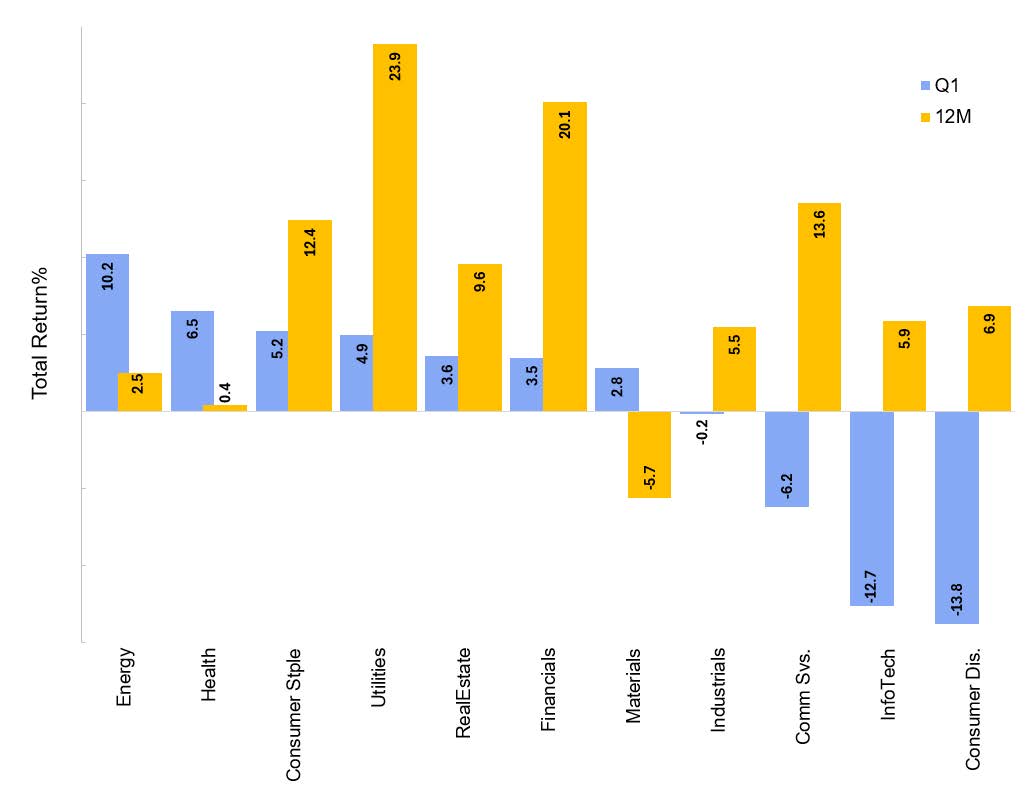

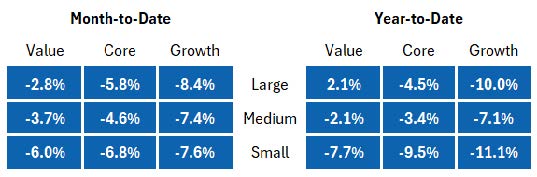

Uncertainty dominated investor sentiment, with markets grappling with the potential implications of the new Presidential Administration’s trade policies, particularly around tariffs, and their effects on the global economy. Inflation remained above target levels, while geopolitical risks began to overshadow last year’s optimism surrounding AI advancements. As a result, the S&P 500 fell by -4.28%, with notable underperformance in Consumer Discretionary, Information Technology, and Communication Services sectors. The growth-heavy NASDAQ posted a sharp decline of -10.26%. In contrast, the Dow Jones Industrial Average, reflecting more established, value-oriented companies, was down a more modest -0.87%. Mid- and small-cap stocks struggled, with returns of -6.11% and -9.48%, respectively. In a reversal of recent trends, growth stocks lagged behind value stocks as investors recalibrated their expectations in response to higher risks. Developed international markets saw notable outperformance, with stocks rising by 7.03%, as investors turned to relatively undervalued opportunities compared to the more expensive U.S. market. Emerging markets also posted a gain of 2.97%. The DJ Real Estate Index increased by 3.49%, benefiting from the broader rotation out of growth and into value-oriented sectors.

FIXED INCOME MARKETS

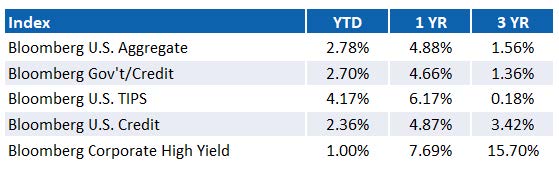

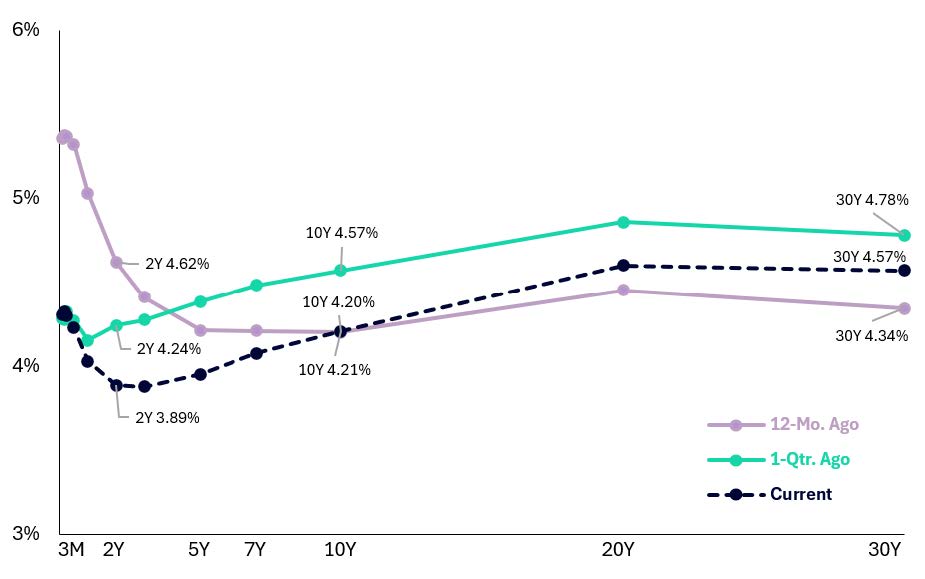

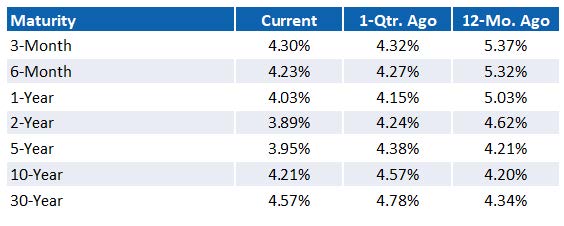

Bond markets posted positive returns across sectors as yields declined in response to tariff uncertainty and concerns over slowing economic growth. Intermediate-term bonds led the rally, with five-year Treasury yields falling nearly 50 basis points as the yield curve disinverted. Fed Funds futures now price in more than two additional rate cuts in 2025. Riskier high-yield and corporate bonds underperformed risk-free Treasuries, as credit spreads widened from historically tight levels—though absolute returns remained positive.

LOOKING AHEAD

As we move into the second quarter of 2025, we continue to maintain our defensive positioning as we navigate ongoing economic headwinds, trade policy concerns, and uncertainty around corporate earnings. By reducing equity weightings ahead of recent market declines and increasing our allocation to developed international markets, we sought to mitigate risk amid lofty U.S. valuations and broader economic challenges. Our increased exposure to gold has helped hedge against volatility, while falling interest rates have supported fixed income markets. In contrast to recent years of concentrated markets, a diversified approach is now offering more stability. While remaining cautious, we are also actively seeking long-term investment opportunities that may arise in this environment. Historically, market corrections have created opportunities for those with a long-term perspective. For instance, the average decline during the worst three-month periods for the S&P 500—dating back to 1950—has been -20.8%, with an average return of 28.5% one year later. While short-term losses can be difficult to manage, staying committed to a long-term investment strategy has often been the best way to weather volatility. We remain committed to helping you navigate these times and ensuring your portfolio stays aligned with your long-term objectives. Please don’t hesitate to reach out to our wealth management team to review your investment goals and ensure your portfolio is properly aligned with your risk tolerance.

MAJOR ASSET CLASS RETURNS

S&P 500 SECTOR RETURNS SIZE & STYLE RETURNS

SIZE & STYLE RETURNS

OTHER

EQUITY INDEX RETURNS

U.S. FIXED INCOME RETURNS

U.S. TREASURY MARKET

Source: Bangor Wealth Management and Bloomberg. Data as of 3/31/2024.

Past performance is no guarantee of future results.

Wealth Management Products:

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

Bangor Wealth Management of New Hampshire LLC is a wholly owned subsidiary of Bangor Savings Bank.