Published on : 10/1/2025

KEY POINTS

- U.S. equities hit record highs in Q3 2025, with the S&P 500 rising 8.1%, rewarding investors who embraced AI’s potential despite economic and geopolitical uncertainties.

- In the first three quarters of 2025, a risk-on sentiment prevailed as economic data exceeded expectations, driving outsized gains in technology stocks, high-yield bonds, and cryptocurrencies.

- The U.S. economy sustained growth in Q3 2025, with GDP rising 3.9% according to the Atlanta Fed GDP Forecast, and consumer spending remaining robust. Tariff-related inflation has had minimal impact so far, prompting the Federal Reserve to cut borrowing costs, with further reductions expected before year-end.

THE ECONOMY

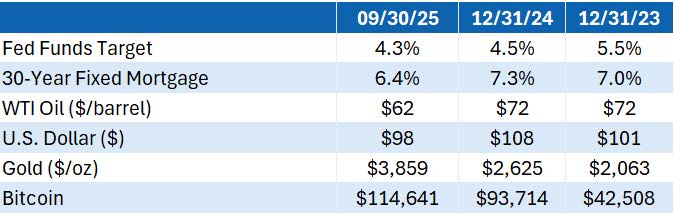

In Q3 2025, the U.S. economy showed signs of continued recovery after the Q1 contraction. Real GDP grew at an annualized rate of 3.9%, according to the Atlanta Fed’s GDP Forecast, compared with the final 3.8% reading for Q2, as both consumer spending and business investment outpaced survey expectations. Core inflation remained above the Fed’s 2% target, with consumer prices rising at an annual rate of 2.9% through August. Producer prices were also elevated, though they came in below forecasts despite tariff concerns. The labor market weakened, adding just 22,000 jobs in August versus expectations of 75,000, while prior data revisions showed employment for the year ending March 2025 was overstated by 911,000 jobs. The unemployment rate ticked up to 4.3% and is projected to reach 4.5% by year-end. In response, the Federal Reserve cut rates to 4.00%–4.25% in September and signaled the possibility of two more reductions before year-end.

GLOBAL EQUITIES

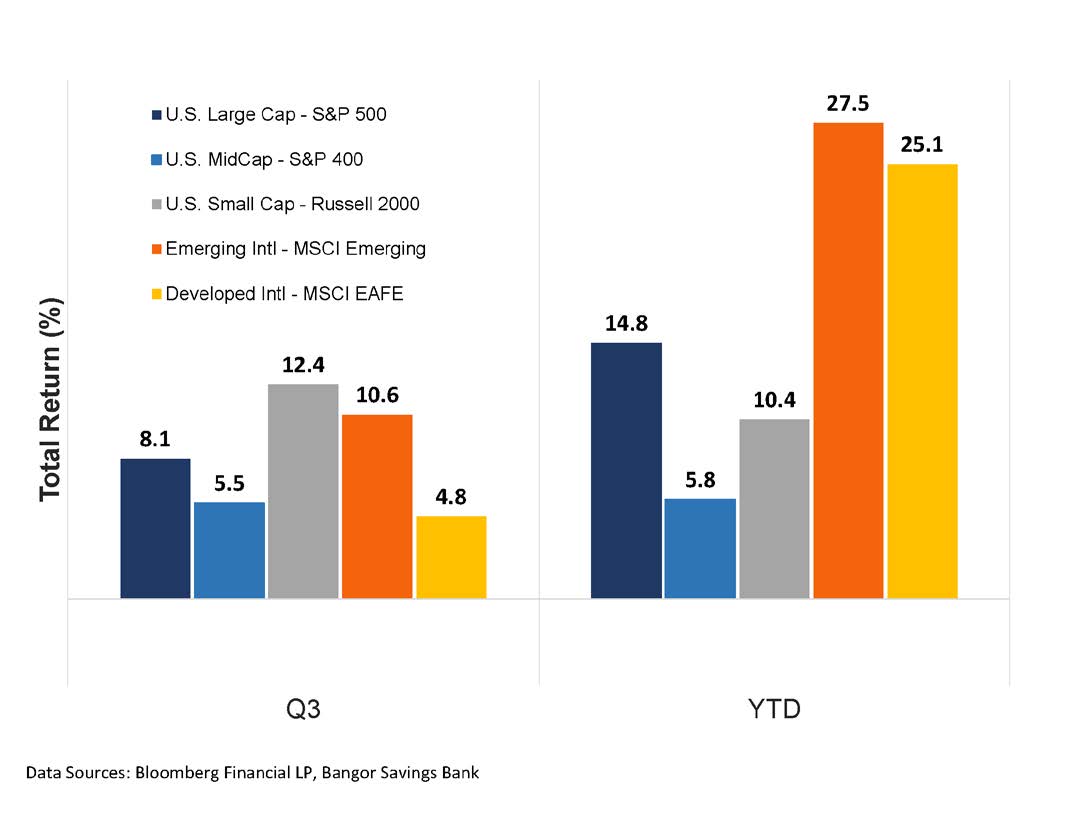

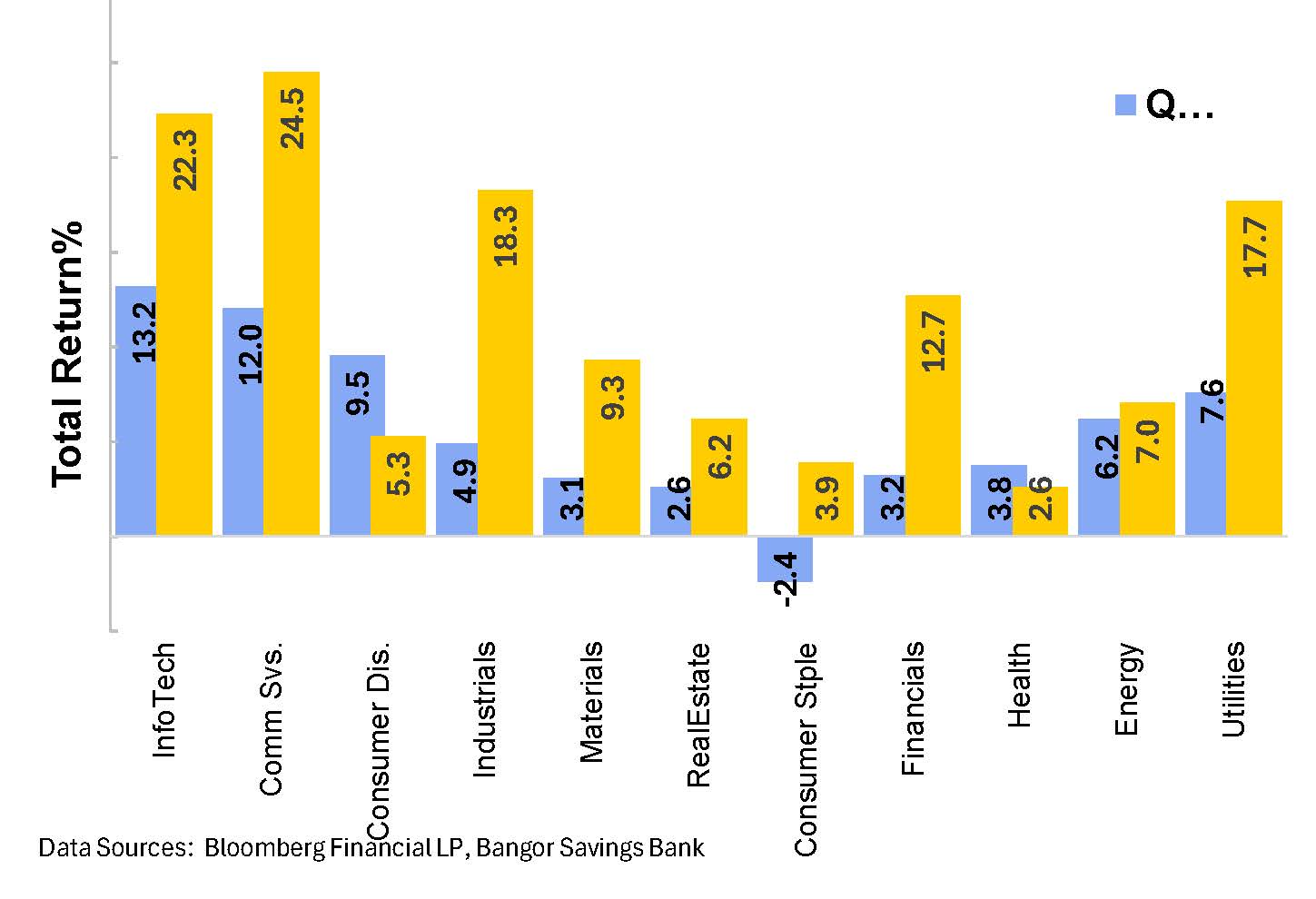

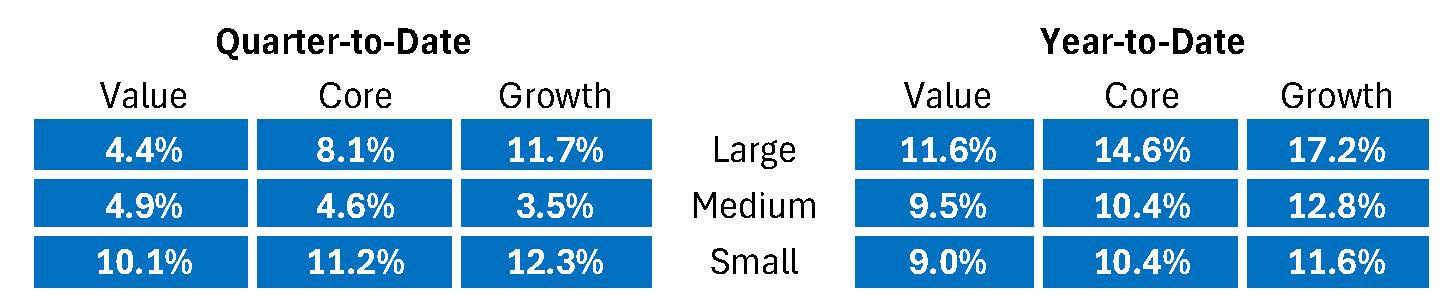

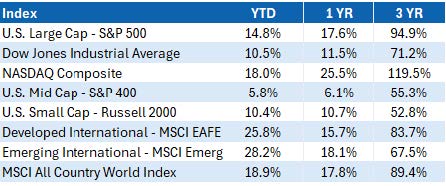

Driven by Artificial Intelligence capital spending, and improving earnings expectations, the third quarter of 2025 was strongly positive for stocks, with the S&P 500 returning 8.1%, and September’s 3.5% return being the best for that month since 2010. Growth equities remained leadership for this quarter, led by Information Technology (+13.2%), Communication Services (+12.0%), and Consumer Discretionary bouncing back as well (+9.5%). The NASDAQ composite returned 11.4%, while the Dow Jones Industrial Average rose 5.7%. Mid- and small-cap stocks posted gains of 5.5% and 12.4%, respectively. International and emerging market equities continued to benefit from attractive valuations, supported by currency tailwinds. Developed markets rose 4.9%, while emerging markets saw another double-digit quarter, returning 10.9%.

FIXED INCOME MARKETS

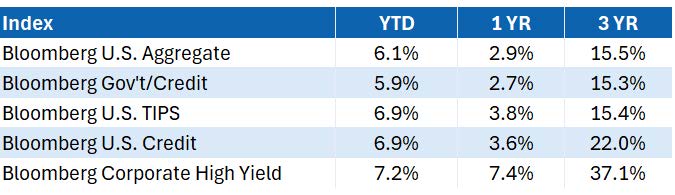

Fixed income markets delivered mostly positive returns in Q3 as bond yields declined on the back of global central bank rate cuts amid slowing economic momentum, particularly in labor markets. The U.S. Treasury Index gained 1.6% for the quarter, extending solid year-to-date performance. Riskier assets outperformed, with Investment Grade Corporates, High Yield, and Emerging Markets debt benefiting from continued spread tightening to historically low levels. In contrast, developed international bonds ex-U.S. lagged, posting modest negative returns due to fiscal pressures, persistent inflation, and ongoing quantitative tightening.

LOOKING AHEAD

In Q3 2025, equity markets delivered strong returns led once again by large-cap technology and AI-related companies, as resilient corporate earnings bested the lingering market concerns over tariffs and inflation. Additionally, a weakening labor market prompted the Federal Reserve to cut rates, further supporting the S&P 500’s double-digit year-to-date gains, while small and mid-cap equity returns were again more muted. While U.S. large-cap technology continues to be leadership-other parts of the portfolio- international equities, short duration fixed income, and gold continue to provide meaningful contributions to overall portfolio returns. This underscores the value of broadly diversified asset allocations, especially amidst market turbulence and ongoing domestic and geopolitical uncertainties. However, equity market price/earnings multiples remain quite elevated, especially in mega-cap technology, leaving markets vulnerable to earnings or policy disappointments, and therefore, we are cautious in our overall outlook. Most notably, the upcoming meeting between President Trump and President Xi in South Korea at the end of October, as well as the Supreme Court’s review of the legality of tariffs in early November, are very important near-term catalysts that could influence the economy, corporate confidence, and global supply chains. As always, we remain focused on helping you achieve your financial goals, in accordance with your long-term investment strategy and risk tolerance parameters. Therefore, please don’t hesitate to reach out to our wealth management team to review your investment goals and to ensure your portfolio is positioned appropriately.

MAJOR ASSET CLASS RETURNS

S&P 500 SECTOR RETURNS SIZE & STYLE RETURNS

SIZE & STYLE RETURNS

OTHER

EQUITY INDEX RETURNS

U.S. FIXED INCOME RETURNS

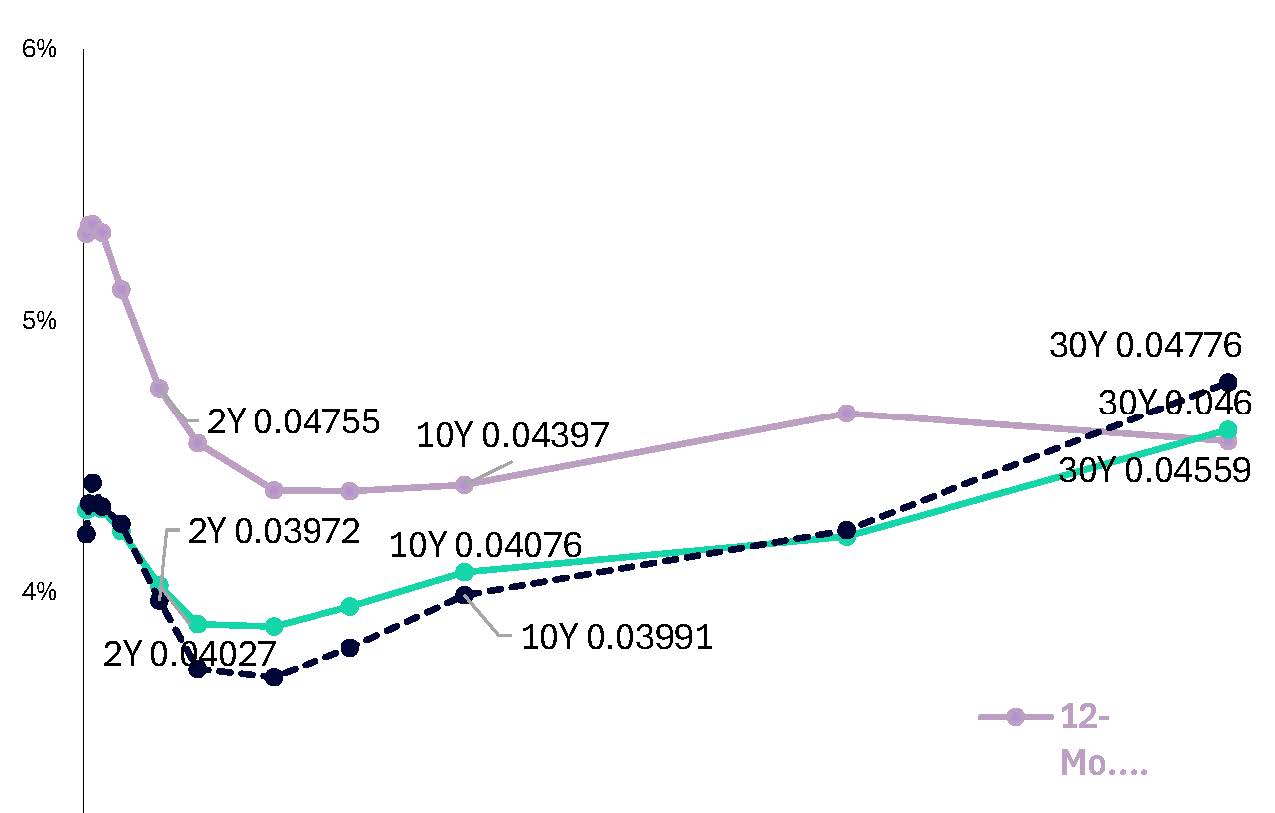

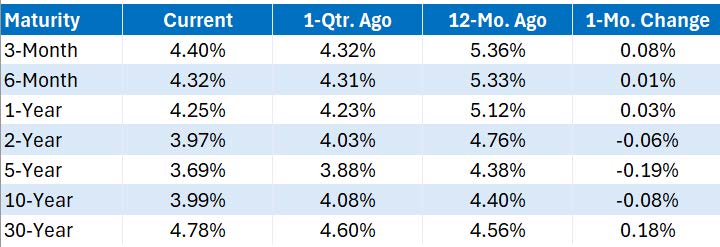

U.S. TREASURY MARKET

Source: Bangor Wealth Management and Bloomberg. Data as of 9/30/2025.

Past performance is no guarantee of future results.

Wealth Management Products:

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

Bangor Wealth Management of New Hampshire LLC is a wholly owned subsidiary of Bangor Savings Bank.