Published on : 3/31/2026

KEY POINTS

- Domestic and global equities posted negative returns in the first quarter, with investors rotating towards defensive assets as geopolitical risks resurfaced

- Fixed income markets were volatile amid elevated commodity prices and persistent inflation concerns, resulting in modestly negative returns for the quarter

- Economic data showed resilient consumer spending and labor market conditions, as well as resurgent inflationary pressures, thereby complicating the Federal Reserve’s path regarding future monetary policy

THE ECONOMY

In the first quarter the U.S. economy showed continued positive momentum supported by moderate consumer spending and a resilient though uneven labor market. Inflation continued to ease from prior peaks but remained well above target, constraining the Federal Reserve’s ability to pivot toward further easing of monetary policy. With GDP data still pending, the quarter is best characterized as one of steady but fragile growth, sensitive to ongoing inflationary pressures and continued geopolitical uncertainty.

GLOBAL EQUITIES

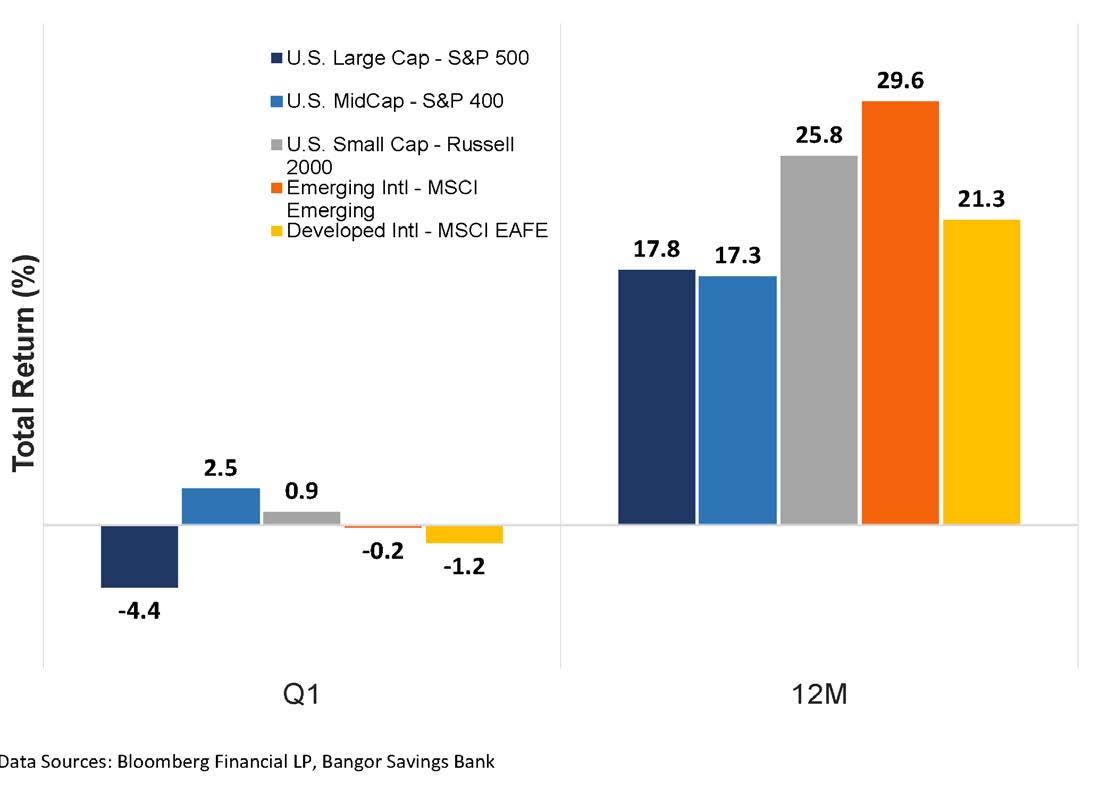

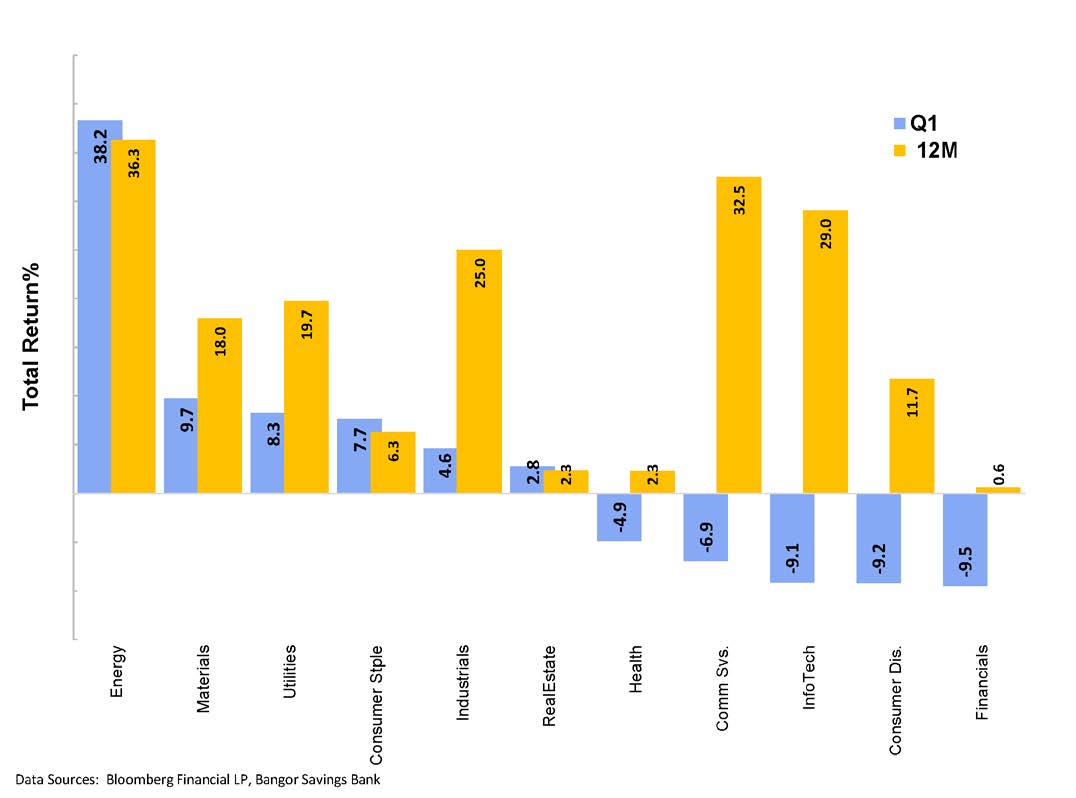

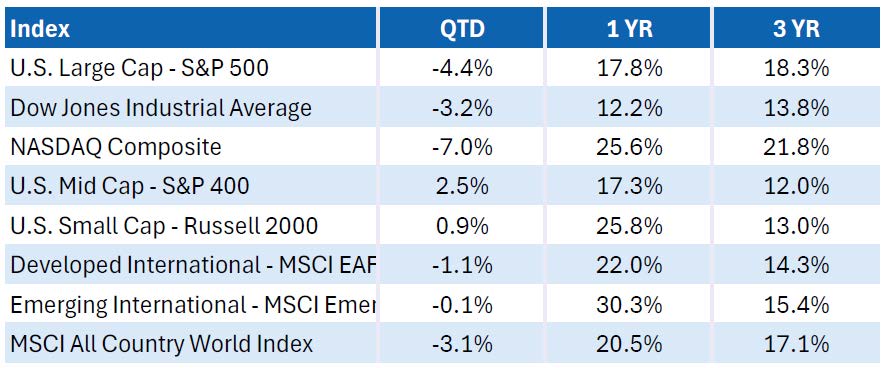

The first quarter of 2026 saw the S&P 500 navigate escalating geopolitical tensions in the Middle East and a spike in oil prices resulting in a -4.4% return for the quarter. Sector leadership shifted toward defensive and real-economy assets, with Energy (+38.2%) leading gains following the closure of the Strait of Hormuz. Other defensive sectors like Utilities and Consumer Staples outperformed, while previous leaders such as Information Technology (-9.1%), Communication Services (-6.9%), and Financials (-9.5%) retraced as the "AI-driven rally" faced valuation pressures. Despite weakness in domestic large-cap equities, market breadth improved with small-cap stocks (Russell 2000) gaining 0.9%, while mid-caps stocks outperformed with a 2.5% gain. International equities also faced similar headwinds from global energy shocks. Developed markets (MSCI EAFE) returned -1.2% while emerging markets were nearly flat at -0.12%.

FIXED INCOME MARKETS

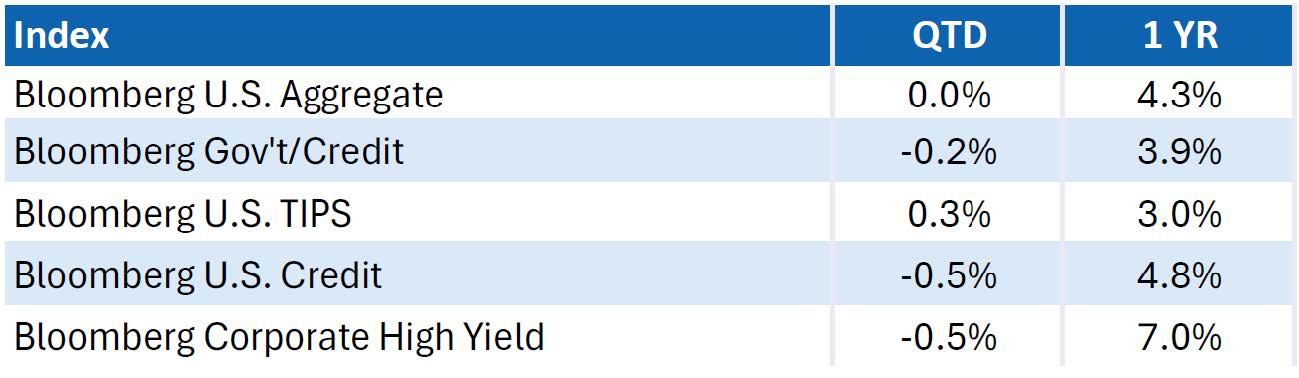

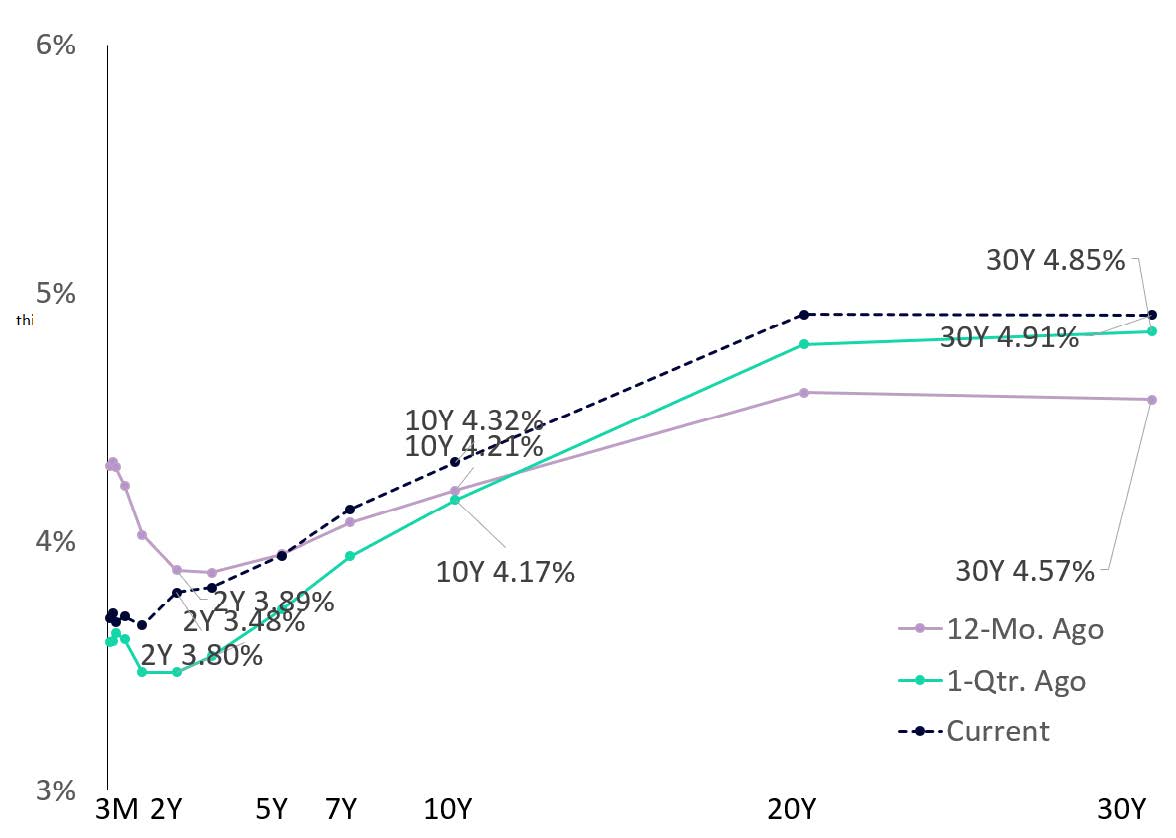

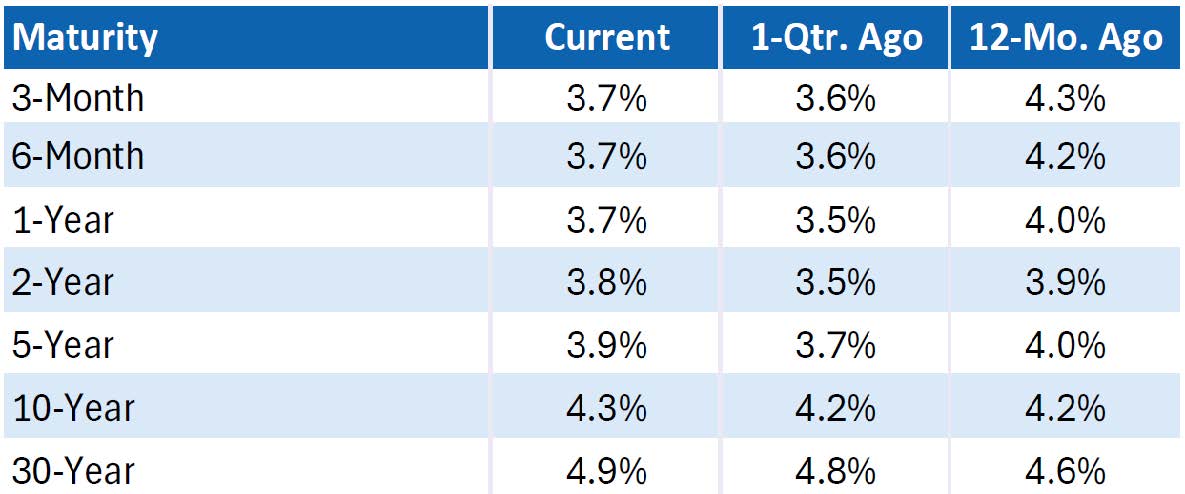

Bond markets were volatile in the first quarter of 2026 as escalating geopolitical tensions—particularly involving Iran—drove energy prices higher, revived inflation concerns, and pushed government bond yields up. The 10-year U.S. Treasury yield rose from about 3.95% to the low 4.4% range, as markets shifted expectations away from rate cuts toward a prolonged Fed pause or the possibility of a tightening of monetary policy. Credit market performance was mixed with higher quality sectors proving more resilient, though all fixed income sectors experienced spread widening. High yield and emerging markets bonds were most impacted amidst a risk-off market sentiment environment. Overall, fixed income returns were flat to modestly negative during the quarter; however, the increase in yields improved their medium-term income generating potential, underscoring bonds’ role as a defensive and diversifying asset class despite ongoing macroeconomic and geopolitical uncertainty.

LOOKING AHEAD

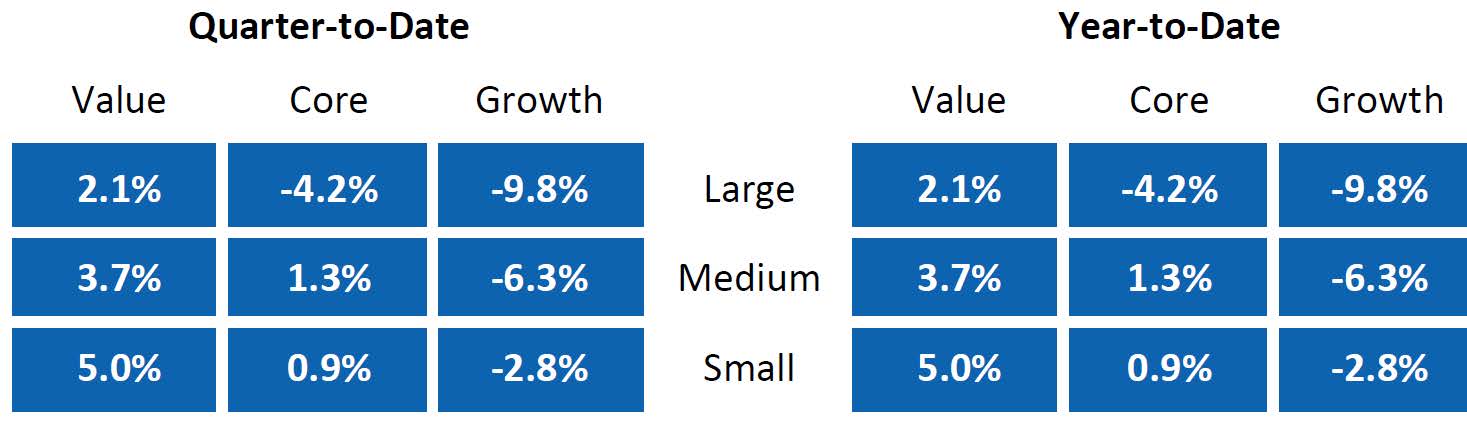

The first quarter of 2026 delivered a notable shift in market dynamics as the multi-year dominance of mega-cap technology stocks began to consolidate. The S&P 500’s 4.4% decline reflected a mild valuation reset following three consecutive years of exceptional double-digit gains. While inflationary pressures from energy markets and shifting Federal Reserve rhetoric contributed to early-year volatility, the underlying market structure remains healthy as market performance continued to broaden beyond the Magnificent 7 into more cyclical and defensive sectors as highlighted by the recent outperformance of the equal weight S&P 500 versus the capitalization weighted benchmark. The relative outperformance of small and mid-cap stocks, as well as international stocks, during the quarter also reinforces our core belief in the importance of broad market portfolio diversification to manage risk and to help you achieve your investment goals.

As always, our investment management focus remains on asset allocation discipline, while simultaneously researching opportunistic, but selective opportunities to benefit from the dislocations in markets. Currently, the trajectory of global energy prices, the Fed’s response to persistent service-sector inflation, and the ongoing fiscal debate in Washington are all very important strategic market themes that inform our investment process. Please reach out to our wealth management team to discuss your investment portfolio and to ensure that it continues to be appropriately positioned given your risk tolerance and investment goals.

MAJOR ASSET CLASS RETURNS

S&P 500 SECTOR RETURNS

SIZE & STYLE RETURNS

EQUITY INDEX RETURNS

U.S. FIXED INCOME RETURNS

U.S. TREASURY MARKET

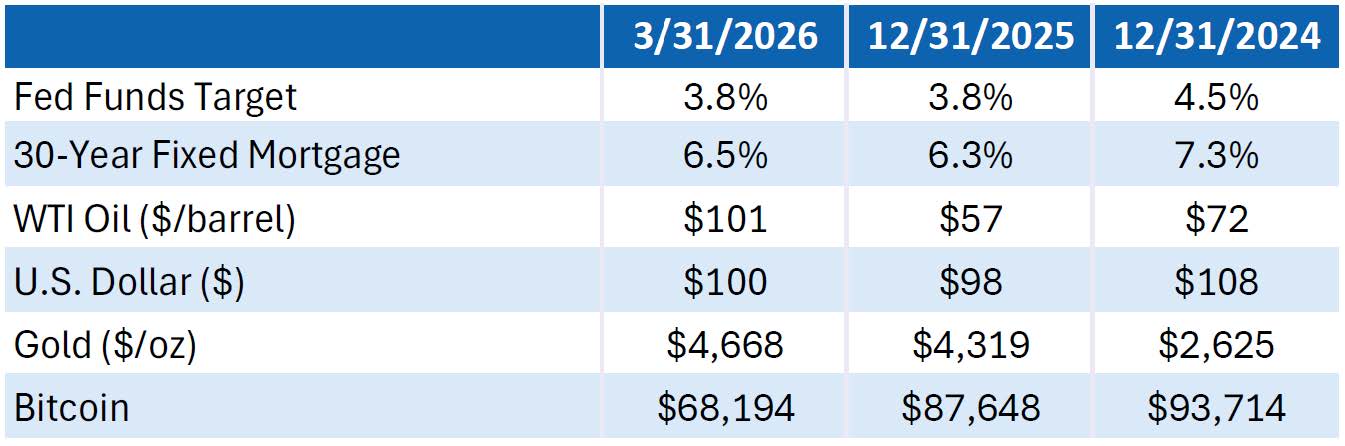

OTHER

Source: Bangor Wealth Management and Bloomberg. Data as of 3/31/2026.

Past performance is no guarantee of future results.

Wealth Management Products:

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

Bangor Wealth Management of New Hampshire LLC is a wholly owned subsidiary of Bangor Savings Bank.