Published on : 1/1/2026

KEY POINTS

- 2024 built on the strong investment performance of 2023, with impressive gains driven by solid earnings and resilient economic growth, despite global uncertainties and high valuations. Investors should anticipate more modest returns in 2025

- AI investments, particularly from the ‘Mag-7’ companies, are expected to exceed $500 billion, fueling long-term productivity and continued economic growth

- The U.S. economy remains resilient with strong consumer behavior and low unemployment. Earnings growth should stay robust, though equities face risks from high valuations, inflation, and geopolitical tensions. Fixed income returns should benefit from the move to higher interest rate

THE ECONOMY

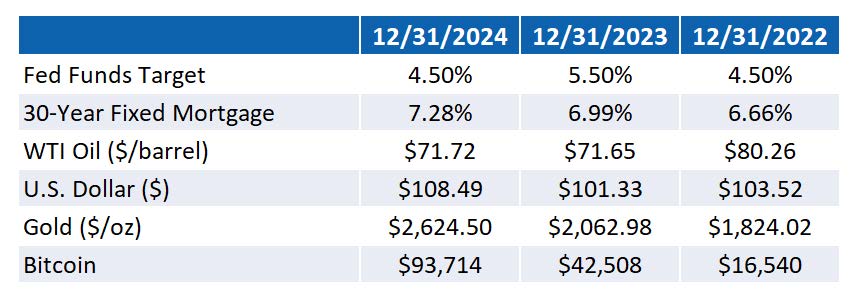

The U.S. economy continued to exhibit above-trend growth and a resilient labor market throughout the year, surpassing most economists’ expectations. Nominal growth remained strong, with gross domestic product (GDP) increasing by 3.1% in the third quarter and expected to moderate only slightly to the mid-2% range in Q4. The unemployment rate edged up by 0.1%, reaching 4.2%, while jobless claims remained historically low. The encouraging inflation metrics observed for much of the year appear to have stalled in the fourth quarter, with most price indices rising marginally, though still well below the highs seen in 2022. Despite ongoing economic strength, the Federal Reserve implemented a 25 basis point rate cut at both meetings in the fourth quarter, while signaling that future rate reductions will likely slow in order to avoid reigniting persistent inflationary pressures.

GLOBAL EQUITIES

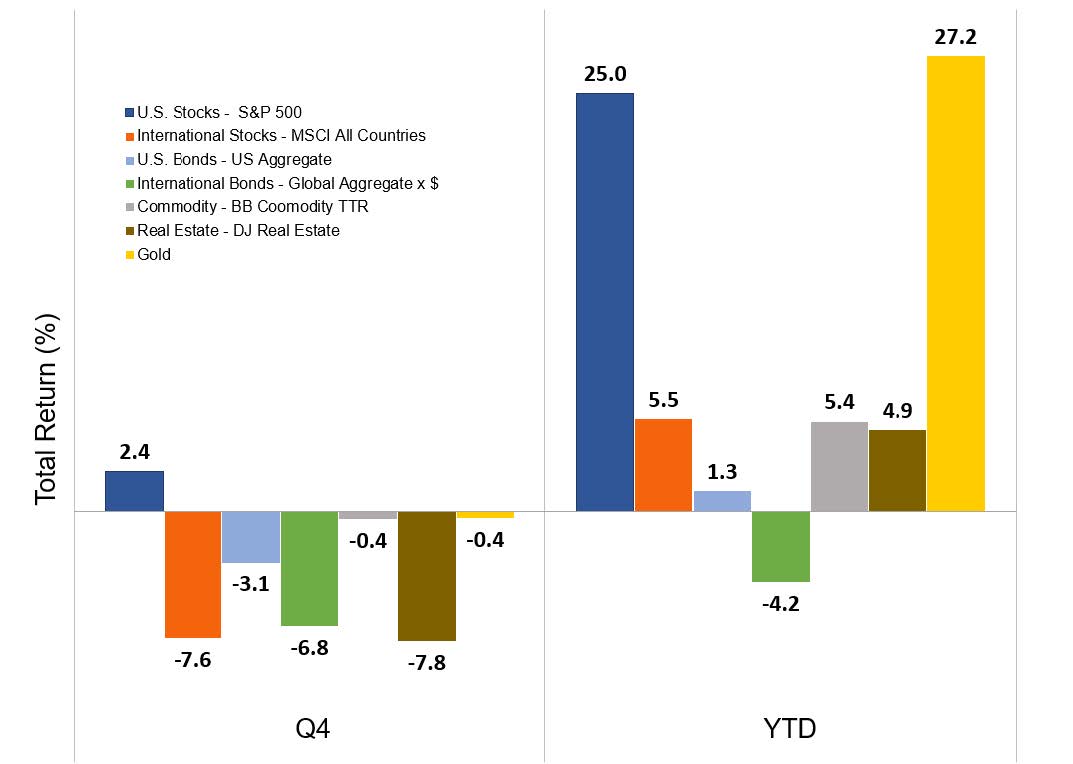

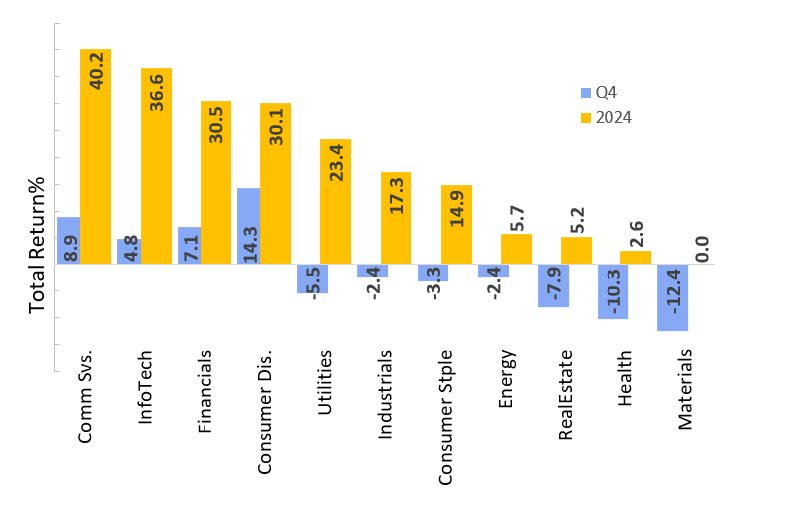

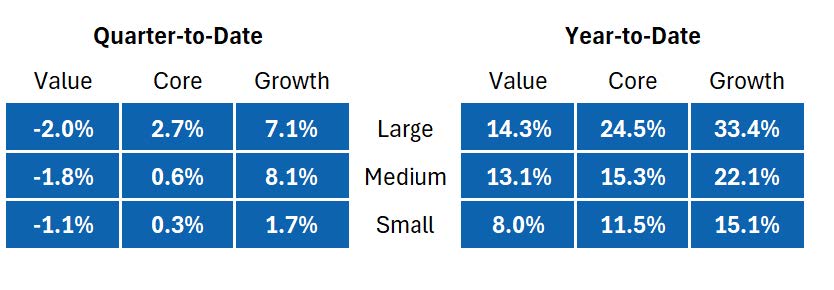

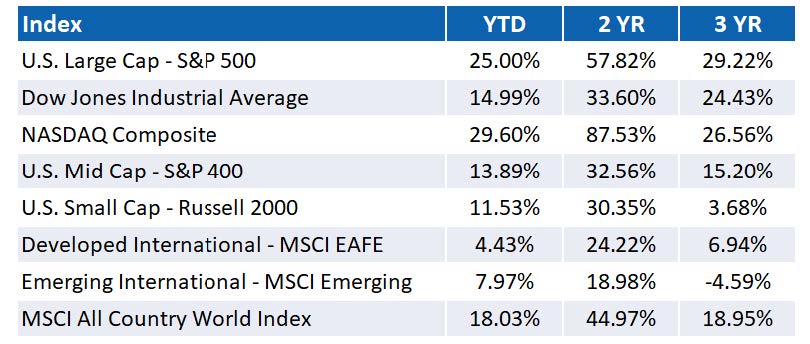

During the fourth quarter of 2024, investors closely examined the impact of the U.S. election results on the markets. Federal Reserve policy remained a key topic of debate, as both inflation and employment data continued to come in stronger than expected. Against this backdrop, the S&P 500 increased by 2.4%, driven by strong performances in the Consumer Discretionary, Financial, and Communication Services sectors. Meanwhile, the growth-heavy NASDAQ posted a return of 6.4%. In contrast, the Dow Jones Industrial Average, which includes more established companies, advanced by just 0.9%. Mid-and small-cap stocks underperformed, each rising by only 0.3%. Growth stocks continued to outperform value stocks, maintaining this overall trend for the year. International markets struggled with ongoing economic and geopolitical challenges, with developed international stocks falling by 8.1%. China’s economic weakness persisted, leading to a 7.9% decline in emerging markets, despite continued government efforts to stimulate the Chinese economy. The DJ Real Estate Index fell by 7.8%, weighed down by elevated interest rates and sluggish performance in the office and retail sectors.

FIXED INCOME MARKETS

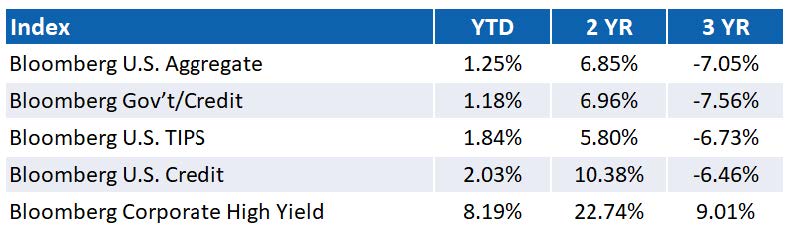

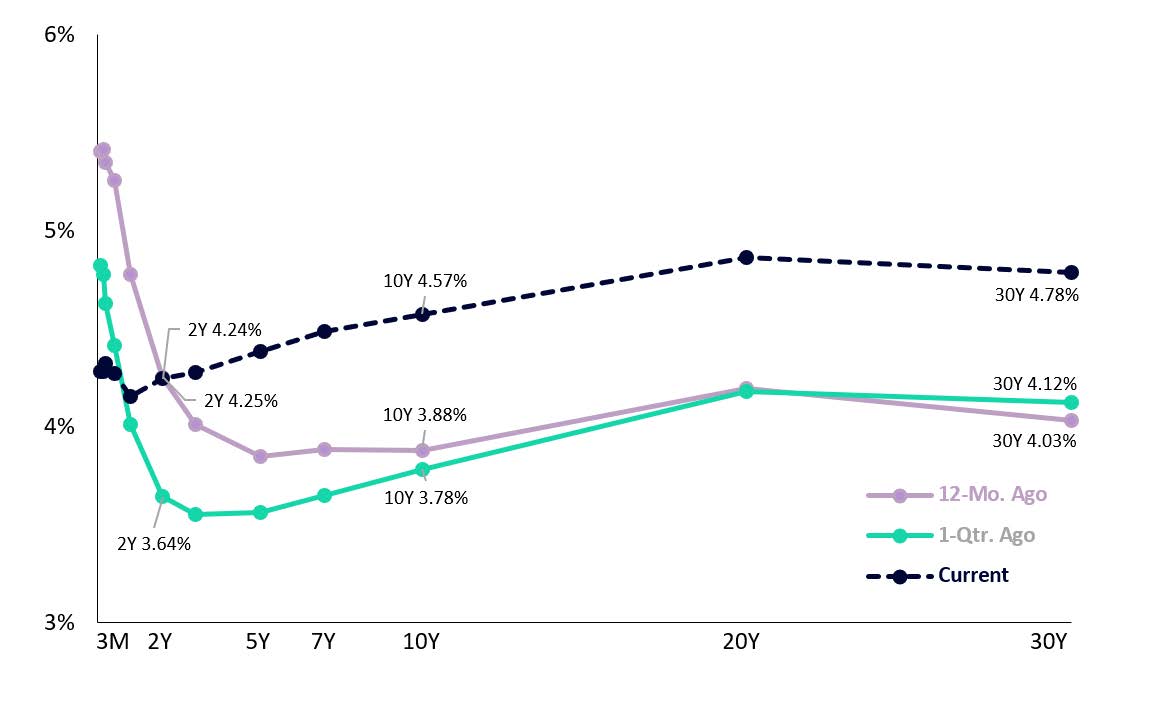

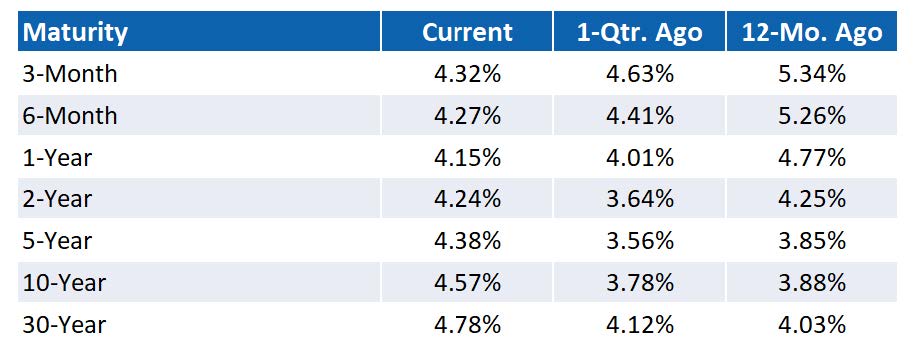

Bond markets experienced negative performance across the asset class throughout the quarter as yields rose, driven by a re-pricing of aggressive Federal Reserve rate cut expectations, concerns over the deficit, and inflation fears. Fixed income yields increased, with longer-dated bonds leading the way as the yield curve steepened. After a multi-year period of an inverted U.S. Treasury curve, it reverted to more historically normal levels, reintroducing a positive term premium. Market-based inflation expectations rose as investors factored in the new administration’s policies and the potential implications of tariffs. Nevertheless, the Fed continued to cut rates at its December meeting but signaled that future cuts would likely slow and become more data-dependent. Despite the negative return for the quarter, fixed income overall posted positive returns for 2024, led by the more volatile sectors, such as high yield (+8.2%) and emerging markets (+6.6%).

LOOKING AHEAD

After two consecutive exceptionally strong years, we expect 2025 investment returns to be more measured. The “Magnificent 7” stocks have driven much of the recent market surge, but with valuations stretched, future gains will likely depend on earnings growth rather than further multiple expansion. While the AI-driven capital expenditure boom has fueled economic growth, those investments will need to translate into meaningful productivity gains to sustain market momentum. A broadening U.S. business cycle, easing global central bank policies, and a more favorable regulatory environment should continue to support equity markets, though risks remain around trade policies, geopolitical tensions, and inflation. In fixed income markets, we believe 2025 presents a favorable backdrop for investors seeking attractive long-term returns amidst potential global volatility. Despite uncertainty, history shows that the best defense against an uncertain investing landscape is having—and sticking with—a long-term financial plan. Please reach out to our wealth management team to review your investment goals and ensure your portfolio aligns with your risk tolerance.

MAJOR ASSET CLASS RETURNS

S&P 500 SECTOR RETURNS

SIZE & STYLE RETURNS

EQUITY INDEX RETURNS

U.S. FIXED INCOME RETURNS

U.S. TREASURY MARKET

OTHER

Source: Bangor Wealth Management and Bloomberg. Data as of 12/31/2025.

Past performance is no guarantee of future results.

Wealth Management Products:

NOT FDIC INSURED | NO BANK GUARANTEE | MAY LOSE VALUE

Bangor Wealth Management of New Hampshire LLC is a wholly owned subsidiary of Bangor Savings Bank.