What Is Credit & Why Do We Need It?

Using credit can be a powerful tool that helps you invest in your future and build a financial life you want. At its most basic credit is a way to borrow money, which can be used to get goods and services now, with the promise to pay later, often with interest. Credit gives you access to money for major expenses like college or home repairs. It also helps you build a financial history, which makes it easier to borrow in the future.

Types of Credit

| Type of Credit | Description | Examples |

|---|---|---|

| Revolving Credit | This type of credit has a maximum credit limit, and you can borrow up to that limit. Each month, you make a payment and if that payment doesn't cover the outstanding balance, you carry the balance to the next month with added interest (or "revolve the debt"). | |

| Installment Credit | With installment credit you are given a lump sum up front. You'll make regular payments to pay back the loan at a fixed amount over a set period of time. |

Credit Facts to Know

- A good credit score can help you qualify for a loan, but it's only one factor lenders consider. Lenders also consider income, debt-to-income ratio, employment history, and other factors before approving a loan.

- Deposit accounts in good standing do not affect credit score but can play a factor in qualification.

- The longer your credit accounts stay open — and are used responsibly — the more your credit score can grow.

- A low credit score reflects past credit history, not your worth or morality. Many factors—like medical debt or job loss—can impact credit without indicating irresponsibility.

- Closing a card can negatively impact your score by reducing your available credit and increasing your credit utilization ratio. Keeping old accounts open often helps with your score but should still be closed to mitigate chances of fraudulent activity which may go unseen on old, unused accounts.

- Responsible credit use can help you build a strong financial foundation and may access better rates on loans.

- Carrying a balance does not improve your score and costs you interest. Instead, aiming to pay your balance in full each month is best for your credit and your wallet.

Credit Scores

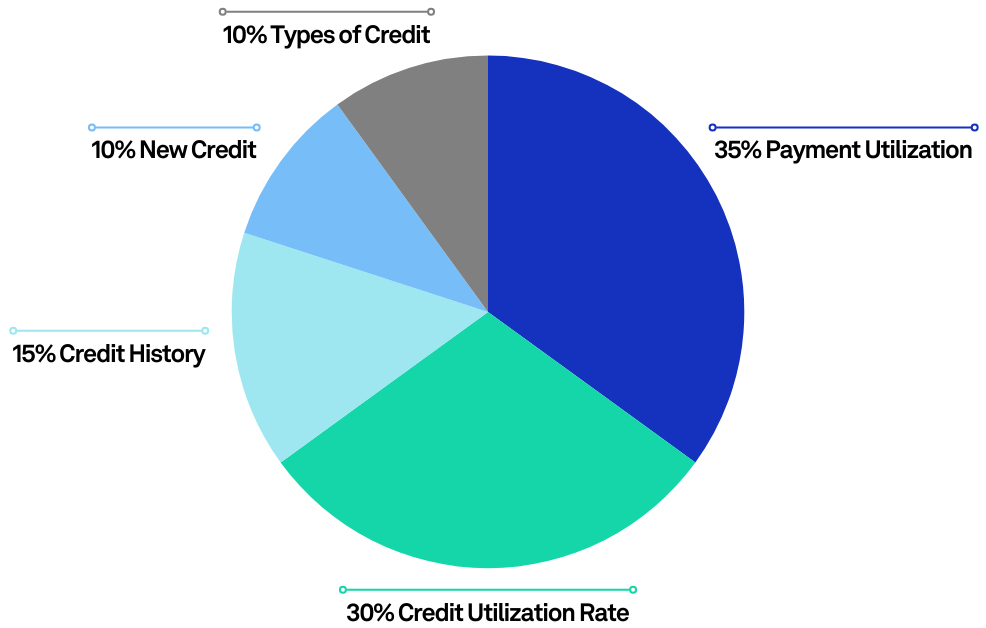

Your credit score is created with a complex algorithm that takes multiple factors into consideration. The breakdown below shows what factors into a credit score calculation:

Breakdown of Your Credit Score

- Payment History/Payment Utilization= 35%

- Paying bills on time is an essential best practice for a healthy credit score.

- Amounts Owed/Credit Utilization Rate= 30%

- Strive to use less than 30% of your available credit. For example, with a credit limit of $1,000, use only $300 at a time.

- Borrow only what you can comfortably repay.

- Credit History = 15%

- The longer your accounts are in good standing, the better.

- New Credit= 10%

- Open new credit lines only when necessary. Limiting the use of credit can benefit your score.

- Types of Credit Used= 10%

- Maintain a healthy mix of revolving and installment credit lines.

A Note on “Consumer” Credit Reports

- Some credit card companies or credit bureaus will provide your credit score within their online tools. These scores may or may not be calculated using a different algorithm than the typical FICO score. Therefore, you will find credit scores vary between the three bureaus (Equifax, TransUnion, and Experian).

Best Practice

Check your credit regularly at annualcreditreport.com for errors or inaccurate information.

How Interest Works

Understanding how interest works helps you recognize the true cost of borrowing, which can empower you to make informed decisions that support a strong financial future.

Note: The costs and interest rates of your loans will vary depending on your lender and the terms and conditions of your loan.

Let’s start with a definition: Interest is an amount a lender charges for borrowing money, usually shown as a percentage of the loan.

For example, let's say you'd like to borrow $5,000 with an interest rate of 5% APR to be paid back in a year. At the end of the year when you've paid off the loan, you'll have paid back the original amount of $5,000, plus roughly $133 in interest. If there are upfront fees of the loan, they may increase the amount paid.

Note: Your loan may be calculated differently based on various factors including the type of loan.

Interest on Credit Cards

Credit cards also have interest but are calculated slightly different. For credit cards, interest is applied on balances that are carried over month-to-month. If you pay the full balance of your credit card by the due date, you will avoid paying interest; otherwise, interest will apply to the entire balance.

For more information on how your loan or credit card payment is calculated, contact your bank or creditor.

Action Steps You Can Take Today

- Annually review your credit report on annualcreditreport.com and dispute any errors

- Consider freezing your credit with each credit bureau if you don't plan to open new credit in the near future

Continue Your Financial Wellness Journey

Next Module: Save for the Future

Previous Module: Build Your Emergency Savings

Overview: Your Financial Wellness Journey

Credit Products from the Bank You Trust

Whether you’re looking for credit cards with world-class features and local support, a mortgage from New England’s lender of choice, or personal loans with competitive rates, flexible terms, and convenient payments, start your journey with your trusted community bank.1